Embarking on a journey often brings excitement and anticipation, but it also necessitates careful planning, especially regarding unforeseen circumstances. A vital part of this preparation is understanding your travel insurance policy. Knowing precisely when does travel insurance start and end is not merely a detail; it’s a critical aspect that determines the scope and effectiveness of your protection. This knowledge ensures you are adequately covered from the moment you commit to your trip until your safe return, addressing potential financial losses or medical emergencies. Therefore, understanding when does travel insurance start and end for your specific policy is paramount for peace of mind.

Understanding Your Travel Insurance Coverage Start Dates

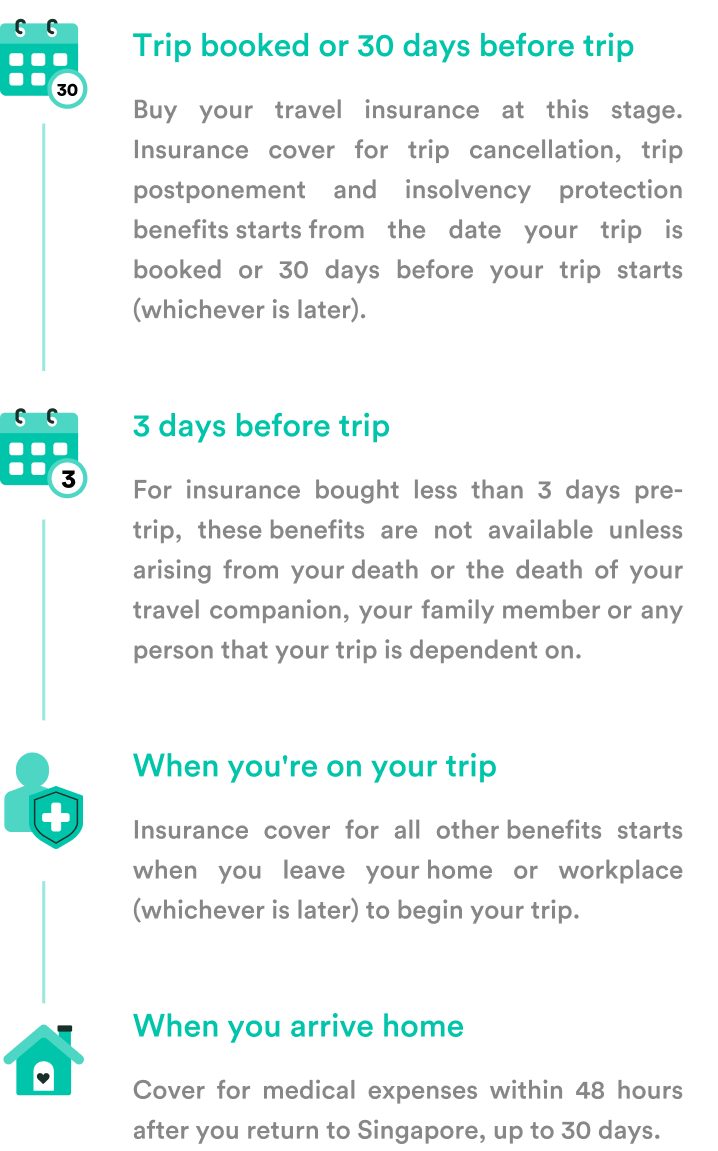

The initiation of your travel insurance coverage isn’t always as straightforward as the day you depart. Different components of your policy may activate at varying times, offering protection for distinct phases of your trip. It’s crucial to distinguish between these activation points to maximize your benefits.

Immediate Protection: When Travel Insurance Begins Right Away

Some aspects of travel insurance policies are designed to offer immediate protection, often kicking in shortly after you purchase the policy, even if your trip is months away. This immediate activation is particularly beneficial for certain types of coverage.

- Trip Cancellation Coverage: This is perhaps the most common example. If you purchase a policy with trip cancellation benefits, this coverage typically begins the day after you buy the policy. This means if you have to cancel your trip due to a covered reason (e.g., illness, natural disaster, job loss) before you even leave, you could be reimbursed for non-refundable expenses like flights and hotel bookings.

- Trip Interruption Coverage (Pre-Departure): While often associated with events during the trip, some aspects of interruption coverage might activate early, covering events that force you to cut your trip short before it even properly begins.

Delayed Activation: When Coverage Kicks In Later

Conversely, many core benefits of a travel insurance policy do not activate until your trip officially commences. This is typically tied to your departure date or the start of a specific travel segment.

- Medical Emergency Coverage: Protection for medical emergencies, hospital stays, and emergency evacuation usually begins on your scheduled departure date. It covers incidents that occur while you are away from home.

- Baggage Loss/Delay Coverage: This benefit typically starts when you begin your journey, usually when your luggage is checked in or when you board your first flight. It covers loss, theft, or delay of your personal belongings during transit and at your destination.

- Travel Delay Coverage: Benefits for flight delays, missed connections, or other travel interruptions generally become active on your scheduled departure date, providing reimbursement for unexpected expenses incurred due to these delays. It’s essential to clarify with your provider precisely when does travel insurance start and end for different benefits.

Navigating the End of Your Travel Insurance Policy

Just as important as knowing when your coverage starts is understanding its conclusion. Travel insurance policies are finite and have specific termination points. Misinterpreting these can leave you exposed just when you think you’re still protected.

The Standard Conclusion: When Travel Insurance Ends Upon Return

For most single-trip travel insurance policies, the coverage ceases upon your return to your home country or city. This is usually defined as reaching your primary residence.

- Scheduled Return Date: Policies are typically structured to end on your scheduled return date, or a set number of hours (e.g., 24-48 hours) after you arrive back at your home address. This allows for potential delays or final transit issues.

- Maximum Trip Duration: Even if you return earlier, the policy will not extend beyond its stated maximum trip duration (e.g., 30, 60, 90 days).

Extending Your Protection: What If Your Trip Changes?

Life and travel are unpredictable. Sometimes, trips get extended, or unforeseen events cause delays beyond your original planned return. What happens to your insurance then?

- Automatic Extensions: Many policies include a short grace period or an automatic extension clause for unforeseen and unavoidable delays that prevent you from returning home on time (e.g., flight cancellations, natural disasters). This extension typically covers a few days and is usually limited to the event that caused the delay.

- Voluntary Extensions: If you decide to extend your trip purely for leisure, you generally need to contact your insurance provider before your original policy expires to request an extension. This may involve additional premiums and a re-evaluation of your coverage. Not all policies allow for voluntary extensions, so always check the terms and conditions.

Frequently Asked Questions About Travel Insurance Timelines

Understanding the intricacies of travel insurance start and end dates can be complex. Here are some common questions to help clarify the process.

Can I buy travel insurance after my trip has already started?

Generally, no. Most travel insurance policies require you to purchase coverage before your departure date. If you buy a policy after your trip has commenced, it typically will not cover any incidents that occurred before or during the initial days of the policy’s activation. Some specialized “post-departure” policies exist but often come with restrictions and waiting periods.

What if my flight is delayed past my policy end date?

Many policies offer an automatic extension for a short period (e.g., 24 to 48 hours) if your return is delayed due to circumstances beyond your control, such as flight cancellations, severe weather, or airline mechanical issues. This ensures you remain covered until you can reasonably return home. Always check your policy wording for specific details on automatic extensions.

Does travel insurance cover me during a layover?

Yes, your travel insurance typically covers you during layovers, provided they are part of your continuous journey to your destination or back home. This includes medical emergencies, baggage issues, and travel delays that occur during the layover period. However, if you intentionally plan a multi-day stopover, you should ensure your policy covers the entire duration of each segment.

What if I have an annual multi-trip policy? When does it start and end?

For annual multi-trip policies, the policy itself starts on the purchase date (or a specified start date) and ends one year later. However, the coverage for each individual trip within that year still adheres to the single-trip rules: cancellation benefits start on purchase, and other benefits activate upon departure for each trip and cease upon your return from each trip. Each trip must also adhere to the maximum trip duration specified in the annual policy (e.g., no single trip can be longer than 30 days).

Grasping the nuances of when does travel insurance start and end empowers travelers to make informed decisions and ensures they are never caught off guard. By carefully reviewing your policy documents and understanding the specific activation and termination points for various benefits, you can embark on your adventures with greater confidence and the assurance that your investment in travel protection truly serves its purpose. Always read the fine print and consult with your insurance provider if you have any questions or unique travel plans.